GameStop's Q1'20 earnings show a substantial $177 million comprehensive net loss due to COVID-19 closures, high expenses, and reduction in tax assets.

Retailer GameStop isn't doing well right now. The company was already on a shaky foundation, and the weeks-long COVID-19 closures put a serious dent in net income, and under-performance has diminished one of the company's most valuable assets: Deferred taxes.

GameStop's net sales for the Q1'20 period were $1.021 billion, down 34% year-over-year. But this is just revenue. After expenses, the company reported a total operating loss of $108 million, compared to a positive $17.5 million in Q1'19. The simple reason for this is GameStop spent more than it made.

GameStop made $1.021 billion in Q1'20, but it spent $738.6 million in cost of sales. That leaves a gross profit of $282.4 million. But after subtracting $386.5 million it spent on selling, general, and administrative expenses, which includes the $18.5 million it spent to help buffer out-of-work wages for employees, GameStop posted a negative operating loss.

After adding in interest fees and tax asset reduction, total income losses were at $165 million.

A big portion of this loss was due to a $53 million drop in tax asset value due to a valuation allowance adjustment.

"Net loss of ($165.7) million, or ($2.57) per diluted share, including a $53.0 million non-cash tax charge associated with the valuation allowance against deferred tax assets," reads the report.

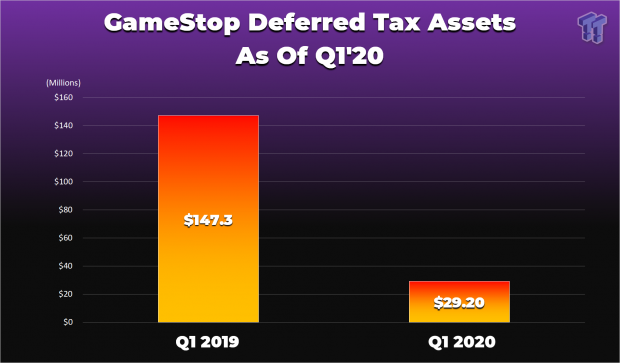

As a result, deferred income tax assets are down significantly, as reflected in the net income loss. In May 4, 2019, GameStop had $147.3 million in deferred income tax assets. On May 2, 2020, that value dropped 80% to just $29.2 million.

This is seen as an asset because GameStop can use these deferrals to lower the taxable income across multiple years. It's good news when a company has deferred taxes because they're a kind of saved boon for later use.

The deferrals arise when companies like GameStop reports a financial loss, which it has for many quarters since October 2018. When a company reports a loss, they can do something called a tax loss carryover, which can be claimed for later tax relief. Carryovers usually last for 7 years.

This deferred tax asset gets adjusted over time in an special account called an allowance valuation account.

The deferred tax valuation gets adjusted as a company makes or loses money. If it makes more money, the carryover taxes can be used to offset the profits and lower total income taxes for that period. Companies will save and use the carryover deferred taxes when they perform a drastic turnaround in generated income.

If it makes less, which GameStop has in Q1'20, the asset is adjusted (subtracted from the asset balance sheet). The deferred taxes aren't a cash charge but the perceived loss in value, which in this case, are recorded as part of the operating income loss.

GameStop doesn't see a payoff for all its deferred taxes

So what does this mean? Essentially GameStop carved off a portion of the deferred taxes because it doesn't see a point in the future where it'll be able to use them. The company telegraphs that it doesn't see a big turnaround any time soon that would warrant the deferred tax usage.

Total assets are also down 32% from last year to $2.469 billion due to significantly reduced inventory. GameStop reduced its inventory by $494.4 million due to coronavirus disruption. So not only were net sales down, but total inventory was significantly reduced.

The loss grows as GameStop recognizes $12.1 million from foreign currency transition adjustments, which is a typical subtraction every quarter.

All-told GameStop reported a total comprehensive loss of $177.8 million.

Even with these losses, GameStop isn't going under any time soon. The company says it expects to have enough liquidity to push forward with its 2020 restructuring plan, which sees a new push towards digital and the remodeling of its stores.

GameStop plans to double down hard into digital and further reduce story inventory by 43%. It notes that e-commerce sales were up 1400% as more consumers buy goods online versus in-store, but this is to be expected given the store close-downs.

Sony discloses financial results for 2025, takes huge loss on Bungie, PS6 release date still undecided

Sony discloses financial results for 2025, takes huge loss on Bungie, PS6 release date still undecided Koei Tecmo sells 14 million games in FY25 due to Pokopia, NiOh 3 success, sales up 84% over last year

Koei Tecmo sells 14 million games in FY25 due to Pokopia, NiOh 3 success, sales up 84% over last year EA heavily slashes earnings targets as Dragon Age, FC25 underperform, shares drop by 16%

EA heavily slashes earnings targets as Dragon Age, FC25 underperform, shares drop by 16% Final Fantasy XVI and Rebirth weren't enough to stabilize Square Enix's operating losses

Final Fantasy XVI and Rebirth weren't enough to stabilize Square Enix's operating losses Ubisoft is optimistic for Assassin's Creed: Shadows despite confirming more layoffs

Ubisoft is optimistic for Assassin's Creed: Shadows despite confirming more layoffs RAM crisis is getting worse, Valve engineer warns

RAM crisis is getting worse, Valve engineer warns Xbox's return to exclusives was decided 'very early on' by CEO Asha Sharma

Xbox's return to exclusives was decided 'very early on' by CEO Asha Sharma Xbox console exclusives can include multiplayer games too

Xbox console exclusives can include multiplayer games too Assassin's Creed Black Flag Resynced sells over 3 million copies, New Game+ is coming

Assassin's Creed Black Flag Resynced sells over 3 million copies, New Game+ is coming Modder plays GTA Vice City and GTA III on a TV inside GTA San Andreas

Modder plays GTA Vice City and GTA III on a TV inside GTA San Andreas Enthusiast puts 11 fans and an AiO on an RTX 3080, gains only 4 FPS

Enthusiast puts 11 fans and an AiO on an RTX 3080, gains only 4 FPS Spotify removed 75 million AI-generated tracks in 2025 as it cracks down on royalty abuse

Spotify removed 75 million AI-generated tracks in 2025 as it cracks down on royalty abuse YouTuber claims Sony is using social media bots to push back against backlash over its physical disc announcement

YouTuber claims Sony is using social media bots to push back against backlash over its physical disc announcement Apple's first OLED iPad mini could launch as early as October

Apple's first OLED iPad mini could launch as early as October Ryzen 7 7700X3D outperforms Ryzen 7 5800X3D with just one stick of DDR5, making AM4 a terrible option for your next build

Ryzen 7 7700X3D outperforms Ryzen 7 5800X3D with just one stick of DDR5, making AM4 a terrible option for your next build SteelSeries Arctis Nova 7 Wireless Gen 2 Headset Review - New and Improved, But Is It Enough?

SteelSeries Arctis Nova 7 Wireless Gen 2 Headset Review - New and Improved, But Is It Enough? AMD Ryzen 7 7700X3D Review - Days of Future Past

AMD Ryzen 7 7700X3D Review - Days of Future Past Samsung 990 2TB SSD Review - Ninth Gen QLC at PCIe Gen4 Speeds

Samsung 990 2TB SSD Review - Ninth Gen QLC at PCIe Gen4 Speeds ASUS ExpertBook Ultra (Panther Lake) 14" Business Laptop Review

ASUS ExpertBook Ultra (Panther Lake) 14" Business Laptop Review ASUS ROG Raikiri II Xbox Wireless Controller Review - Ready to Take Control

ASUS ROG Raikiri II Xbox Wireless Controller Review - Ready to Take Control MOZA FMP18 Panel Bundle Review: authentic F/A-18 Hornet cockpit controls for flight sims

MOZA FMP18 Panel Bundle Review: authentic F/A-18 Hornet cockpit controls for flight sims Micron 6600 ION 245.76TB Enterprise SSD Review - Best in Class Programming Speeds

Micron 6600 ION 245.76TB Enterprise SSD Review - Best in Class Programming Speeds MOZA MA3F EFCM Flight Control Module Review: authentic Airbus A320 autopilot panel for simulators

MOZA MA3F EFCM Flight Control Module Review: authentic Airbus A320 autopilot panel for simulators Turtle Beach Stealth Pro II Wireless Gaming Headset Review - Premium Sound, Fantastic Features

Turtle Beach Stealth Pro II Wireless Gaming Headset Review - Premium Sound, Fantastic Features MOZA MGX1000 Instrument Panel Review: a realistic Garmin G1000 replica for immersive flight sims

MOZA MGX1000 Instrument Panel Review: a realistic Garmin G1000 replica for immersive flight sims I use this decade-old free tool that finds files faster than Windows Search does

I use this decade-old free tool that finds files faster than Windows Search does I install and update most of my apps with this Windows command now, and I stopped downloading sketchy installers

I install and update most of my apps with this Windows command now, and I stopped downloading sketchy installers Hisense U6SF 65-inch MiniLED TV: High Performance Meets Leisurely Convenience

Hisense U6SF 65-inch MiniLED TV: High Performance Meets Leisurely Convenience I stopped digging through Windows menus after I set up this one folder

I stopped digging through Windows menus after I set up this one folder Don't sell your Windows laptop until you do these things

Don't sell your Windows laptop until you do these things 6 PC cleaning mistakes to avoid for safer hardware maintenance

6 PC cleaning mistakes to avoid for safer hardware maintenance Phison and Intel Take Aim at Local AI's Memory Wall with aiDAPTIV

Phison and Intel Take Aim at Local AI's Memory Wall with aiDAPTIV How to Remap Keyboard Keys in Windows using Microsoft PowerToys

How to Remap Keyboard Keys in Windows using Microsoft PowerToys 7 tips to organize your Windows files for faster, easier access

7 tips to organize your Windows files for faster, easier access Intel Arc G3 Extreme first impressions with MSI's Claw 8 EX AI+ - Incredible power for an extreme price

Intel Arc G3 Extreme first impressions with MSI's Claw 8 EX AI+ - Incredible power for an extreme price