Jon Peddie Research has pushed out a new report for the GPU market in Q3 2022, with the biggest drop in GPU shipments since the 2009 recession.

GPU and CPU shipments dropped significantly year-over-year by 19% with GPU seeing a compound growth rate of 2.8% between 2022-2026, where they'll see an install base of 3.1 billion units at the end of JPR's forecast period. In the next 5 years, JPR predicts discrete GPUs inside of PCs will hit 26%.

Looking at the year-to-year total GPU shipments, these numbers aren't good: they're down 25.1% for all types of platforms and GPUs, while desktop graphics cards dropped 15.4% and notebooks by 30% which is huge: the largest since the 2009 recession. Who lost the most? AMD.

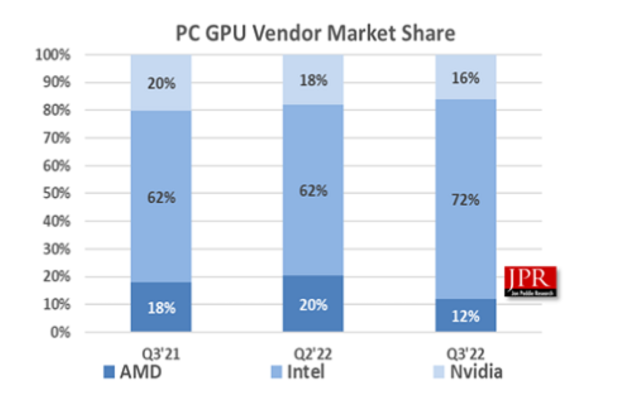

AMD bled out GPU market share of 8.5% during Q3 2022, NVIDIA's GPU market share dropped 1.87% while Intel increased its GPU market share thanks to the Arc GPU launching, seeing Intel GPU market share jump by 10.3% in Q3 2022.

Moving onto overall GPU shipments, they decreased by 10.3% from the previous quarter... but get this: AMD GPU shipments dropped by a rather significant 47.6%, NVIDIA GPU shipments dropped by a smaller 19.7%, while Intel GPU shipments increased by 4.7%.

JPR notes that the third quarter normally sees the biggest growth over the second quarter, but Q3 2022 was down 10.3% from Q2 2022, which means we've dropped below the 10-year average of 5.3%.

Quick highlights

- The GPU's overall attach rate (which includes integrated and discrete GPUs, desktop, notebook, and workstations) to PCs for the quarter was 115%, down -6.0% from last quarter.

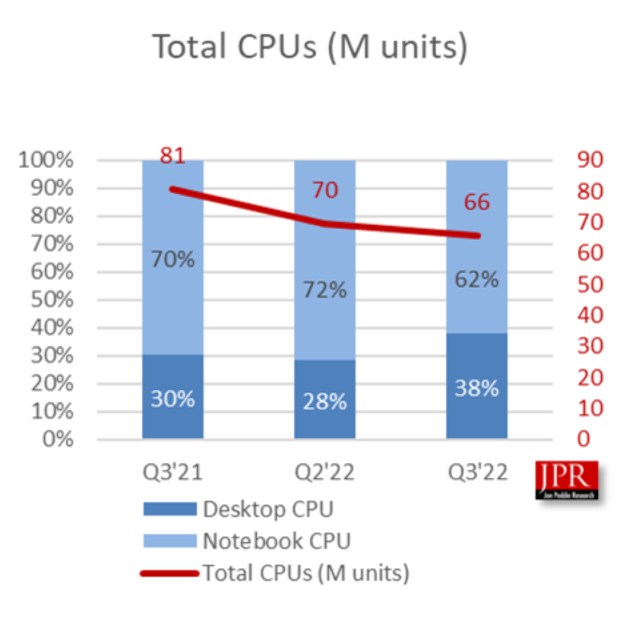

- The overall PC CPU market decreased by -5.7% quarter to quarter and decreased -by 18.6% from year to year.

- Desktop graphics add-in boards (AIBs that use discrete GPUs) decreased by -33.5% from the last quarter.

- This quarter saw 0.5% change in tablet shipments from last quarter.

Jon Peddie noted in the new report: "The third quarter is usually the high point of the year for the GPU and PC suppliers, and even though the suppliers had guided down in Q2, the results came much below their expectations".

"All the companies gave various and sometimes similar reasons for the downturn: the shutdown of crypto mining, headwinds from China's zero-tolerance rules and rolling shutdowns, sanctions by the US, user situation from the purchasing run-up during Covid, the Osborne effect on AMD while gamers wait for the new AIBs, inflation and the higher prices of AIBs, overhang inventory run-down, and a bad moon out tonight".

"Generally, the feeling is Q4 shipments will be down, but ASPs will be up, supply will be fine, and everyone will have a happy holiday".

GPU shipments in Q3 2024 dip, as gamers wait for NVIDIA's new GeForce RTX 50 series GPUs

GPU shipments in Q3 2024 dip, as gamers wait for NVIDIA's new GeForce RTX 50 series GPUs JPR's quarterly GPU shipment report: Q2 2024 shipments up 1.8%, NVIDIA GPU share increases 2%

JPR's quarterly GPU shipment report: Q2 2024 shipments up 1.8%, NVIDIA GPU share increases 2% Desktop GPU shipments hold steady in Q1 2026 with NVIDIA maintaining 90% market share

Desktop GPU shipments hold steady in Q1 2026 with NVIDIA maintaining 90% market share Is there hope for Intel's desktop GPUs yet? Arc graphics cards hit market share milestone

Is there hope for Intel's desktop GPUs yet? Arc graphics cards hit market share milestone GPU shipments hit 76.9 million units in Q4 2024, before Blackwell and RDNA 4 were released

GPU shipments hit 76.9 million units in Q4 2024, before Blackwell and RDNA 4 were released Wizards of the Coast president to leave position as Magic: The Gathering hits record $500M earnings

Wizards of the Coast president to leave position as Magic: The Gathering hits record $500M earnings NVIDIA GeForce driver 610.88 launches without a resolution for Battlefield 6 Season 4's crashing issues

NVIDIA GeForce driver 610.88 launches without a resolution for Battlefield 6 Season 4's crashing issues TCL debuts Ultimate Pro 32X3B and 27X3B gaming monitors with LG's 4th-gen WOLED panel

TCL debuts Ultimate Pro 32X3B and 27X3B gaming monitors with LG's 4th-gen WOLED panel Apple will offer the iPhone and Apple Watch for $17.99 and $11.99 per month

Apple will offer the iPhone and Apple Watch for $17.99 and $11.99 per month Memory supply could plummet 70% as AI's endless hunger devours global production

Memory supply could plummet 70% as AI's endless hunger devours global production Valve fixes Steam bug that downloaded games online instead of over your local network

Valve fixes Steam bug that downloaded games online instead of over your local network World's first tri-mode 1300Hz gaming monitor and 12K ultrawide confirmed

World's first tri-mode 1300Hz gaming monitor and 12K ultrawide confirmed MOZA's first full-cockpit HMA150 motion system adds a new dimension to flying or racing

MOZA's first full-cockpit HMA150 motion system adds a new dimension to flying or racing Anthropic gives thoughts on open-weights models, especially those from China

Anthropic gives thoughts on open-weights models, especially those from China Xbox explains why its massive outage locked players out of games they owned

Xbox explains why its massive outage locked players out of games they owned Logitech G316 X 98 Wired Gaming Keyboard Review - Retro-Inspired Board that Falls a Little Short

Logitech G316 X 98 Wired Gaming Keyboard Review - Retro-Inspired Board that Falls a Little Short Biwin M560 2TB SSD Review - Best Overall Retail-Ready DRAMless SSD

Biwin M560 2TB SSD Review - Best Overall Retail-Ready DRAMless SSD Logitech G512 X 98 Analog Mechanical Gaming Keyboard Review - An Innovative Two-in-One

Logitech G512 X 98 Analog Mechanical Gaming Keyboard Review - An Innovative Two-in-One Thrustmaster T.Flight HOTAS 5 MSFS Edition Review

Thrustmaster T.Flight HOTAS 5 MSFS Edition Review SteelSeries Arctis Nova Pro Omni Wireless Headset Review - One Headset to Rule Them All

SteelSeries Arctis Nova Pro Omni Wireless Headset Review - One Headset to Rule Them All SteelSeries Arctis Nova 7 Wireless Gen 2 Headset Review - New and Improved, But Is It Enough?

SteelSeries Arctis Nova 7 Wireless Gen 2 Headset Review - New and Improved, But Is It Enough? AMD Ryzen 7 7700X3D Review - Days of Future Past

AMD Ryzen 7 7700X3D Review - Days of Future Past Samsung 990 2TB SSD Review - Ninth Gen QLC at PCIe Gen4 Speeds

Samsung 990 2TB SSD Review - Ninth Gen QLC at PCIe Gen4 Speeds ASUS ExpertBook Ultra (Panther Lake) 14" Business Laptop Review

ASUS ExpertBook Ultra (Panther Lake) 14" Business Laptop Review ASUS ROG Raikiri II Xbox Wireless Controller Review - Ready to Take Control

ASUS ROG Raikiri II Xbox Wireless Controller Review - Ready to Take Control Printer Not Working in Windows? How to fix detection, print queues and drivers

Printer Not Working in Windows? How to fix detection, print queues and drivers The Ultimate Guide to Personalizing Your Windows 11 Taskbar

The Ultimate Guide to Personalizing Your Windows 11 Taskbar How to Turn Your Windows Laptop Into a Second Monitor with Miracast and Wireless Display in Minutes

How to Turn Your Windows Laptop Into a Second Monitor with Miracast and Wireless Display in Minutes 6 Mistakes to Avoid When Buying a Windows Laptop

6 Mistakes to Avoid When Buying a Windows Laptop I capped Windows Update's bandwidth with Delivery Optimization, and my downloads stopped choking

I capped Windows Update's bandwidth with Delivery Optimization, and my downloads stopped choking I use this decade-old free tool that finds files faster than Windows Search does

I use this decade-old free tool that finds files faster than Windows Search does I install and update most of my apps with this Windows command now, and I stopped downloading sketchy installers

I install and update most of my apps with this Windows command now, and I stopped downloading sketchy installers Hisense U6SF 65-inch MiniLED TV: High Performance Meets Leisurely Convenience

Hisense U6SF 65-inch MiniLED TV: High Performance Meets Leisurely Convenience I stopped digging through Windows menus after I set up this one folder

I stopped digging through Windows menus after I set up this one folder Don't sell your Windows laptop until you do these things

Don't sell your Windows laptop until you do these things